Entertainment

20-Year-Old Canadian Winner Sparks Debate After Choosing $1,000-a-Week-for-Life Over $1 Million Lump Sum

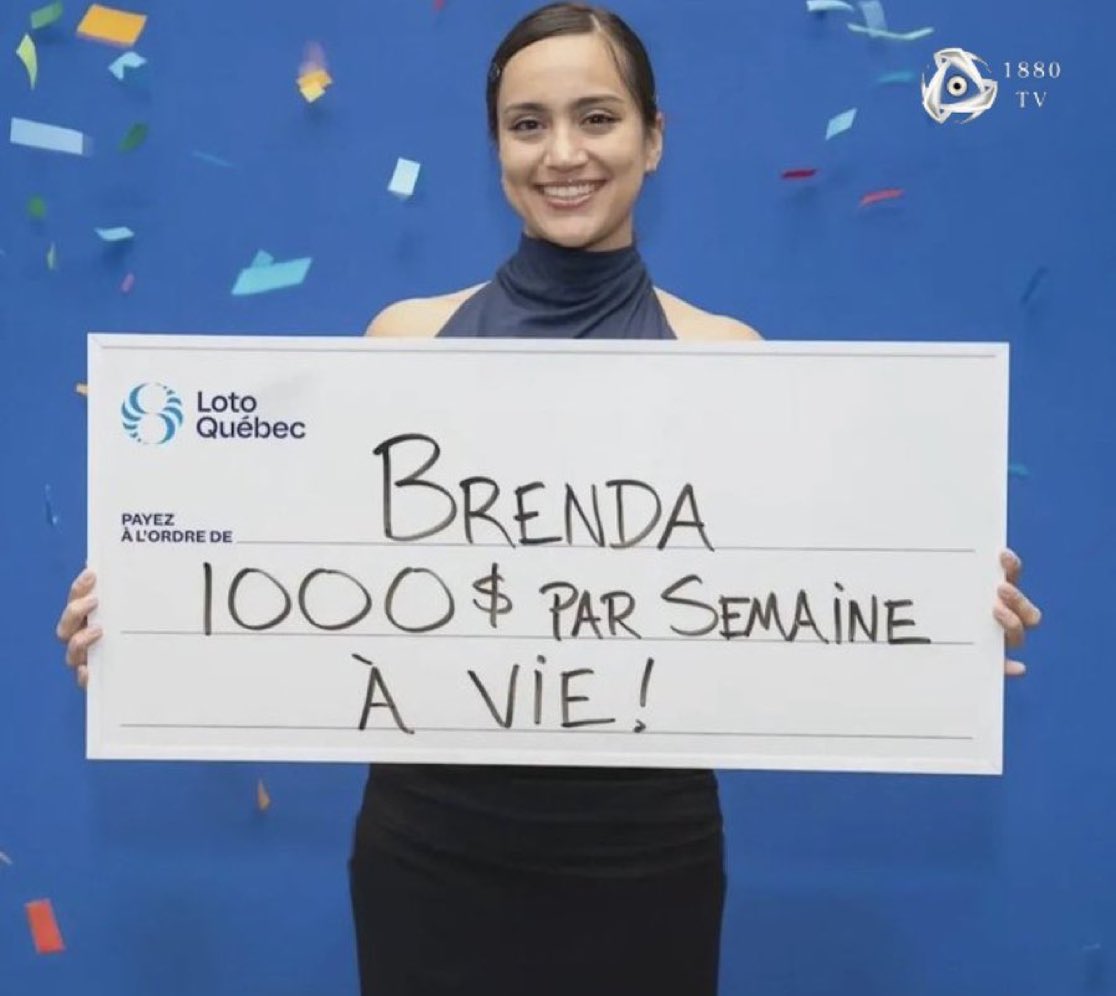

When 20-year-old Brenda Aubin-Vega walked into the Loto-Québec office in July 2025 to claim her “Gagnant à vie” jackpot, she was smiling like someone whose world had just split open into possibilities. But her decision—turning down a $1 million lump sum for $1,000 every week for the rest of her life—quickly set the internet on fire, igniting one of the year’s biggest discussions about money, youth, and the psychology behind sudden wealth.

In a country where lottery winnings are tax-free and young adults are buried under record housing prices, Brenda’s choice struck a nerve far beyond Montreal.

Her decision meant she would earn $52,000 every year for life, a guaranteed income that could stretch beyond $3 million over six decades, assuming she lives to Canada’s average life expectancy. For Brenda, that steady flow of tax-free money felt like a railing she could grip as she climbed toward long-term goals, especially buying a home in Quebec’s notoriously competitive real-estate market. She said she wanted “stability, not pressure,” a statement that resonated with thousands of young Canadians who feel financially squeezed in an economy where ownership seems increasingly out of reach.

But once the news hit social media, the reactions split sharply down ideological lines. Supporters, many of them young and financially cautious, argued she had made a brilliant decision. They pointed to decades of data showing that 70% of lottery winners worldwide run out of their fortune within seven years, especially those who take big lump sums they’re unprepared to manage. People recalled stories of winners who bought mansions, cars, and boats in a rush of excitement—only to end up bankrupt, depressed, or embroiled in family conflicts. For them, Brenda choosing lifetime income wasn’t boring; it was wise, calculated, and emotionally grounded.

But the critics came in louder waves. Investment enthusiasts, financial analysts, and armchair economists insisted she had made a colossal mistake by rejecting the lump sum. The argument was simple: with a diversified investment strategy—index funds, growth stocks, bonds, even modest real-estate ventures—a young person with $1 million today could turn that money into a fortune worth many millions more. They cited long-term market returns averaging 7–10% annually. With compound interest working at full strength over 40 or 50 years, Brenda could have been worth more than $10 million by mid-life. Social media feeds filled with calculators and graphs showing the “true cost” of choosing fixed payments that don’t grow, especially under inflation.

Inflation became the centerpiece of the debate. While $1,000 weekly feels huge at age 20, many critics pointed out how the value of money shrinks over time. With Canada’s historical inflation rate hovering around 2–3% annually, the real purchasing power of Brenda’s weekly payment could be cut in half by her 50s. What feels like steady income today could become modest pocket money decades later in a world where prices will almost certainly be higher. One user summarized it bluntly: “She locked herself into a salary that gets worse every year.”

Still, others pushed back, arguing that ordinary people—even ambitious ones—struggle with managing large sums. A 20-year-old suddenly holding $1 million faces intense social pressure, predators, missteps, and emotional impulses very few are equipped to handle. Taking the weekly income gives her peace of mind, a financial rhythm, and protection from disastrous decisions or manipulative acquaintances. Some noted that Brenda now has something many adults chase for decades: a lifetime safety net. She can work when she wants, go to school without debt, buy a house without suffocating stress, and avoid the psychological burnout that comes with rapid wealth.

The debate also touched on culture. Canadians, more risk-averse and socially cautious than Americans, statistically prefer structured payments. In Quebec especially, financial conservatism runs deep. Many locals said Brenda’s choice reflected the province’s values: stability over gamble, long-term certainty over financial high-wire acts. To them, her decision wasn’t naïve—it was mature, especially for someone barely out of her teenage years.

But the critics are still unmoved. They warn that Brenda has unknowingly limited her financial future. They argue that what she gains in emotional comfort, she loses in potential economic freedom. And because the payments stop only at death, they are not transferable to future children or family. A million-dollar lump sum, however, could become generational wealth if handled well.

Yet the deeper truth behind the uproar is simpler: Brenda’s choice forced everyone to confront their own philosophy of money. Some people fear losing wealth more than they desire growing it. Some crave stability; others chase opportunity. Some want guaranteed income; others want the thrill of investment. Brenda’s decision became a mirror—and millions of people suddenly saw themselves in it.

As she continues with her life in Montreal, the noise online fades into background chatter. She still receives $1,000 every Monday. Her routine hasn’t changed, but her future has. She’ll buy her home, she’ll build her life, and she’ll do it without the dread of sudden financial collapse. Whether she missed out on millions or prevented a disaster depends entirely on perspective. But one thing is unmistakably clear: in choosing certainty over speculation, Brenda Aubin-Vega became a global example of how differently people define wealth. And sometimes, the biggest lottery win isn’t the jackpot—it’s the peace that comes with deciding how to use it.

Popular Posts

“Stick to Makeup, Sis”: Daniel Regha’s Fiery Clapback at Tacha Sparks Heated Debate Online

12 Dec, 2025

Kuje Nights Begin: Abuja Court Orders Former Labour Minister Chris Ngige Remanded Over Alleged ₦2.2bn Contract Fraud

12 Dec, 2025

“Even the Privileged Are Tired”: Kiddwaya’s Viral Lament Sparks Nationwide Reactions

12 Dec, 2025Scroll to Top